(Sept 23): Earlier this year, DBS Group Holdings received a thank-you note from a digibank customer in India. A self-employed customer was looking for financial aid towards the end of the Muslim holy month of Ramadan. “My children wanted new clothes for Eid. When I was looking for options, I happened to open my digibank app. I saw the ‘PL’ [personal loan] option, clicked on it and applied. I got the money in my account in two to three minutes. No waiting period. This is the best service ever,” the Indian digibank customer says. DBS’s tagline now is “Live More, Wait Less”, raising the bar for any new digital bank player vying for one of five new digital bank licences offered by the Monetary Authority of Singapore (MAS).

Digibank is DBS’s digital bank launched in India in 2016 and in Indonesia in 2017. It started off as a digital-only bank. In March this year, DBS “subsidiarised” its Indian unit, launching DBS India (DBIL). DBS plans to adopt a phygital strategy, which is also its Indonesian model. During DBS’s FY2018 results briefing in February, CEO Piyush Gupta introduced the phygital concept. “The model we have in Indonesia is what I call a phygital model: It’s digital, but we also have around 40 physical branches,” Gupta said. Now, the phygital model is also being adopted in India, where DBS already has two million to three million digibank customers.

Phygital allows DBS to serve all its customers — large corporates, small and medium-sized enterprises (SMEs) and individual customers — and not just smart millennials. “Since the launch of our locally incorporated wholly-owned subsidiary DBIL in March, we’ve been expanding operations and building greater scale in India through a phygital model to further serve SMEs, as well as large corporates and individual customers. We’ve established over 20 customer touchpoints so far this year — a mix of branches and kiosks — in locations such as Mumbai, Hyderabad, Ahmedabad,” a DBS spokeswoman says.

“We recently started piloting data-driven lending solutions for SMEs. The creation of a full-fledged subsidiary in India allows us to scale up further and bring to customers a more compelling proposition,” Gupta said at the launch of DBIL.

In August, DBS announced that DBIL planned to establish more than 100 customer touchpoints — a combination of branches and e-kiosks — across 25 cities in the next 12 to 18 months. In March, DBIL opened nine branches and extended its reach to Hyderabad, Ahmedabad, Coimbatore, Vadodara, Indore and Ludhiana. In addition, it expanded in cities in which it is already present, through new branches in Andheri in Mumbai, as well as Gurugram and Noida in the National Capital Region. It also opened five branches in unbanked rural centres.

Cost of compliance

See also: ECB asks banks for plans to address AI cybersecurity threats

Meanwhile, in Singapore, the five new digital banking licences — two for digital full banks (DFBs) and three for digital wholesale banks (DWBs) — are the most exciting developments in the local banking scene since the qualifying full bank (QFB) licences were introduced in 1999. Yet, analysts and market watchers are saying that the Singapore market is small, and there are limited products and services that these new banks can offer local consumers and companies. In the meantime, these fledgling virtual banks have to comply with regulations, including capital and liquidity ratios imposed on the local banks and qualifying full banks. In addition, the new banks will also have to comply with antimoney laundering and Know Your Client (KYC) processes.

Bharath Vellore, managing director, Asia-Pacific, at Accuity, believes there is room for new players and they will be able to bring new technologies to the table. “We expect the new entrants to increase competition in lending, particularly to more digital-savvy retail and SME customers, despite the regulatory restrictions. We also expect the digital banks to increase pricing competition for deposits as they become more established and seek to develop their funding bases,” he says.

Compliance is an important aspect of banking operations. The compliance department has to ensure the financial institution operates within its regulatory framework. It starts with the onboarding of customers, cybersecurity, assessing and testing the adequacy of the bank’s policies and equipment, such as security and risk assessment tools. Compliance is also required when disbursing loans, or taking in deposits because of strict regulations pertaining to anti-money laundering, KYC, tax evasion or terrorism funding.

See also: MAS issues consultation paper for new protected cell company corporate structure

Compliance costs are rising because of increasingly stringent checks. Notably, US banks are not allowed to process transactions from countries or individuals that the US has sanctioned. The US Office of Foreign Assets Control warns that if it is discovered that a bank’s compliance programme falls short of meeting the full requirement, the bank is in trouble.

On top of more stringent regulations, retail bank accounts are small and costly, yet banks need them because they are a source of lowcost CASA (current account savings account).

This is where technology comes in. Digitalisation, coupled with artificial intelligence, should be able to reduce costs associated with retail bank accounts. “Two ways that digital banks can differentiate themselves [from traditional banks] in the onboarding process are customer experience and cost. That is where huge cost savings will be seen, and accounts can be opened faster,” Vellore says. “One of the biggest costs areas to differentiate is in compliance, which requires people, technology and operational costs just to comply with regulations.”

According to a United Overseas Bank spokeswoman, its digital bank TMRW’s customer onboarding process is automated and in real time. Customers can authenticate and start transacting within minutes. For compliance solutions, UOB is using BAE Systems Applied Intelligence (formerly Detica).

Sandeep Lal, head of digital bank at DBS, says account opening for a digibank account with limited maximum balances can also be done in minutes via a smartphone. “To make this a full savings account, customers can simply verify their identity with a fingerprint at any of more than 500 cafés and stores or have an agent visit them. We use Aadhaar, a biometrics-enabled government ID, which is used by over one billion people in India,” Lal explains. “We have built our own models, which instantly assess applicants against our criteria, using a range of data that customers offer us,” he says, referring to digibank’s screening and compliance process.

Digitalising bank accounts is important because it could lower costs. “The entire pricing model would depend on the cost structure. The key to transaction banking is the customer experience. Would the new DFB offer a better experience than what is on offer in Singapore?” Vellore wonders.

For more stories about where money flows, click here for Capital Section

Vellore: We expect the new entrants to increase competition in lending

Lal: The key to transaction banking is the customer experience

New digital model

Vellore thinks digital banks and banks with successful digitalisation strategies will be at a huge advantage in the future. “One of the other areas to innovate with the digital proposition is lifestyle services. It means the bank has a record of how people live. People do so many things online, so [transacting through the bank] gives you the power of data, insights into customers’ lifestyle. Can a digital bank’s services be tailored to those needs?” he says.

“Banks have an insight into a customer’s financial profile. If digital banks know which utilities you are paying, insurance premiums and so on, they can build a profile using this data and remind you when your insurance premiums and other payments are due. Reminders are the first layer, advising is the next level, for examples, what’s your best utility plan, suggestions for dining. A digital bank can analyse your transactions and give you advice.”

Indeed, these are the plans that Dennis Khoo, regional head of TMRW Digital Group at UOB, has for TMRW.

TMRW uses data to serve and engage customers. According to Khoo, there is a difference between digital banking and a digital bank. A digital bank with no branch presence has no option but to use data to engage with its customers. Digital banking is part of an omnichannel strategy, where customers use technology for transactions but still require the bank’s advisory and other services for investments and services with higher-value-added components.

“When you serve the digital savvy, you can push suggestions to customers,” Khoo says. For example, TMRW can remind customers to pay bills, collect rent from tenants or inform them that their salaries have been credited. It can eventually propose products — suggest a suitable savings product, for instance — after understanding the customer’s lifestyle.

“With these digital banks coming in, it will drive these innovations and that will push traditional players to raise their game and offerings,” Vellore says.

Fitch Ratings warns that the local banks are likely to face increased competition in lending, “particularly to more digital-savvy retail and SME customers, despite the regulatory restrictions. We also expect the digital banks to increase pricing competition for deposits as they become more established and seek to develop their funding bases,” Fitch says in a report. Even then, this could be an Achilles heel for the new digital banks. “Greater competition in the lending market would benefit customers but could increase risk for banks if they relax their underwriting standards or underprice risk in an attempt to capture or defend market share,” Fitch adds.

On the other hand, it is perfectly feasible for the new digital banks to make Singapore their headquarters, and test products in the city state and its regulatory sandbox before they launch operations and products elsewhere in Southeast Asia.

“We believe the underserved market would be fairly small domestically, as Singa pore is well banked, but it could prove a fertile test-bed for new entrants before they launch operations in more lucrative markets in the region,” the Fitch report states.

Ng Wee Siang, senior director, Asia-Pacific banks, Fitch Ratings, says: “Some of these players would be interested in venturing into a few countries,”

The new DFBs will face deposit caps in the first few years. As the minimum paidup capital increases, deposit ceilings will also rise until the paid-up capital is a minimum of $1.5 billion, when there would be no deposit cap.

Challenges ahead

“In the short term, products will be in the lending front. Funding depends on who the players are, and they are likely to rely on equity. As they develop and progress to digital full banks, they will try to develop their own deposit base,” Ng says. The only way to attract deposits is with pricing, but MAS is mindful of value destruction, he adds.

“The presence of the new digital banks could lead to competition on the deposit front. A lot of these deposits are likely to be non-sticky initially. These new banks have to be very careful how they manage their lending to match funding so that duration mismatches are minimised.”

Vellore says: “The biggest challenge for any firm in getting this licence is to differentiate its offering from the digital bank offerings by the local banks and QFBs. DBS has a solid digital offering and UOB has launched a digital bank. The traditional banking system had adopted digitalisation and the offerings are quite robust.”

This is unlike in markets such as the UK, China and Brazil. He adds: “For challenger banks in the UK, it was easy to differentiate their offerings because the traditional banks [in the UK] had not digitised their banks to that extent.”

MAS requires the new digital banks to demonstrate a path to profitability in their applications. How is digibank doing on this front? “Digibank in India and Indonesia is tracking within our expectations. We have built a critical mass of customers and are building on our capabilities. We plan to be profit-making in the next three to five years,” Lal says.

If the new DFBs and DWBs follow the prescribed timetable of submitting applications by Dec 31, followed by MAS’s awarding of licences by mid-2020, the first new digital bank will be able to start operations by mid-2021. By then, TMRW would have been launched in its third or fourth market and digibank could be about to turn profitable.

Digital banks struggle to turn profi table; AI could be a differentiator

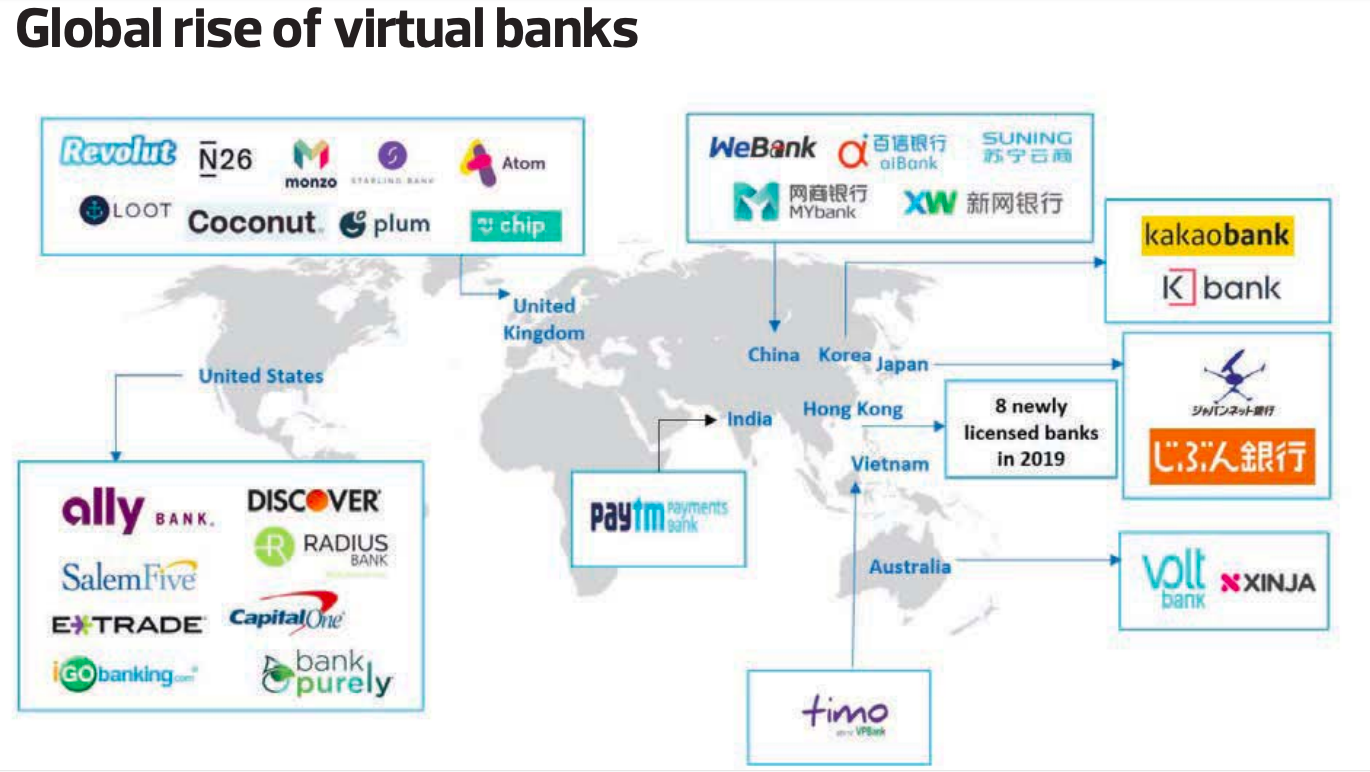

In March, OakNorth Bank, a digital-only bank, announced profit before tax of £33.9 million ($57.9 million) and a profit after tax of £26.6 million for FY2018, up significantly from the profit after tax of £9.5 million reported in FY2017. OakNorth is the only digital bank in the UK that has managed to turn profitable. Others, such as Loot (see chart), have gone into administration. Coconut does not have a proper banking licence; N26 is German, and still loss-making; and Revolut remains loss-making, and has some dissatisfied customers.

Monzo, another digital-only bank in the UK, also remains loss-making. Its strategy revolves around engagement. According to its 2018 annual report, Monzo’s net promoter score (NPS), which measures customer experience and is a gauge for customer loyalty, is +80. It is calculated by subtracting the percentage of detractors from the percentage of promoters. So, to get to +80, 90% of customers must have been happy versus 10% of detractors.

“We’ve grown revenue considerably: we’ve just crossed £40 million of annual run-rate revenue (based on May 2019 revenue), but there’s still plenty of work to do to get to profitability. Around 30% of active users deposit at least £1,000 a month (our definition of ‘salaried’), up from 13% a year ago,” says Monzo CEO Tom Blomfield, in the bank’s 2018 annual report.

Per-user contribution margin (revenue minus variable costs, including expected credit losses) is one of the metrics that Monzo is attempting to improve. This statistic gauges whether each active customer generates more incremental revenue than they create in cost. Monzo calculates that annual per-customer contribution margin is now +£4 as at May 2019, up from -£15 a year ago, and -£65 in 2017.

Dennis Khoo, regional head of TMRW Digital Group at United Overseas Bank, is monitoring some of the scores that Monzo tracks, such as net promoter score, which he says tracks expectations at TMRW, and customer engagement. TMRW uses artificial intelligence. Meniga, developed in its e-Lab, helps customers keep track of their savings and expenses with ease and clarity in real time. Meniga enables TMRW to understand customer needs better and to prompt them to make smarter decisions in managing their finances.

UOB invested in and partnered with Israelbased fintech Personetics, which sifts through data and identifies individual transaction patterns. These insights gained over time can be used to anticipate and prompt customers when their balance may be insufficient to cover upcoming payments, detect unusual or suspicious account activity and highlight opportunities for them to save more or to spend wisely.

In the UK, OakNorth uses its own OakNorth Analytical Intelligence, which has helped ensure that it maintains a high credit quality. OakNorth has not had a single default so far, according to the bank. OakNorth lends to “fast-growth” UK businesses, established property developers and investors, according to its website.

In addition to being profitable, OakNorth’s cost-to-income ratio is 37%, below those of full-service banks such as Singapore’s local banks, which range from 42% to 44%.

As at Dec 31, 2018, OakNorth had shareholders’ equity of £299.3 million, compared with total assets of £1.77 billion and a loan book of £1.3 billion.

Interestingly, OakNorth has a Singapore connection. Last September, it secured US$100 million ($137.7 million) in funding from GIC, Clermont Group, Coltrane Asset Management, EDBI and NIBC Bank. OakNorth started operations in 2015, and an initial investor was Indiabulls, India’s largest non-bank, SME (small and medium-sized enterprise) lender, which invested £66 million. In October 2017, Coltrane, Clermont and Toscafund invested £160 million; in February this year, SoftBank Group’s Vision Fund and Clermont invested US$100 million in total.

KakaoTalk, a virtual bank in South Korea, is also profitable, but its cost-to-income ratio is more than 90%. KaokaoTalk is actually a messaging app that morphed into financial services. KakaoTalk is taking a leaf from Tencent’s book with WeChat, WePay and WeBank. As KakaoTalk is used by 93% of South Korean smartphone users, its financial statements are somewhat different from the likes of Monzo and OakNorth.

The Monetary Authority of Singapore says the entry of new digital players will add diversity and help strengthen the city state’s banking system in the digital economy of the future, and “provide impetus for existing banks to continue enhancing the quality of their digital offerings”. For the new digital banks, there are various models to choose from, including profitable ones.