See also: Analysts mostly bullish on EQDP's impact on SGX; Morningstar views tailwind as ‘temporary’

Yet another record quarterly AUA but analysts split

Despite six consecutive quarters of record assets under administration (AUA) at iFast Corp, analysts remain split on the financial services company.

iFast’s AUA reached $18.38 billion as at Sept 30, up 46.1% y-o-y and 4.8% q-o-q.

Results released on Oct 23 show that its 3QFY2021 (ended Sept 30) net revenue rose 32.6% y-o-y to $30.3 million, while ebit and patmi grew at a slower pace of 22.4% and 23.4% to $9.1 million and $7.5 million respectively, owing to lesser government grants and a net investment loss from debt instruments.

A higher interim dividend of 1.3 cents was declared, compared to 0.8 cents in 3QFY2020.

In an Oct 26 note, UOB Kay Hian Research analyst Clement Ho is maintaining “buy” on iFast with a target price of $11.50, which represents an upside of 24.9%.

“iFast has proven it is able to capture the growing pie of the wealth management industry in its key markets across Asia, driven mainly by the shift towards digitalisation. The longer-term structural dynamics are favourable to iFast as the percentage of managed wealth in Asia grows. This will be driven mainly by China, as financial markets there continue to open and help spur growth in the Asian wealth management industry,” writes Ho.

iFast has several new growth avenues ahead, Ho adds. “These include its Malaysian stockbroking service on the FSMOne.com investment platform to help strengthen the group’s position as a multi-asset investment platform, and help the company move towards its objective of becoming a holistic FinTech platform.”

iFast also has in Hong Kong the development of its eMPF pension platform. “Unfortunately, financial details still cannot be disclosed at this stage. However, iFast did provide its financial targets for 2024–2025 for the overall Hong Kong market. iFast aims to achieve 2024 and 2025 gross revenue of more than HK$1 billion and HK$1.5 billion ($0.17 billion and $0.26 billion) respectively, compared to 2020’s HK$252 million; and 2024 and 2025 net revenue of more than HK$800 million and HK$1.2 billion respectively, compared to 2020’s HK$107 million,” Ho says.

The company is also targeting 2024 and 2025 PBT margins of more than 15% and 33% respectively, compared with 2020’s 30%.

“To recap, the project has a two-year implementation period to be completed by end-2022, and a seven-year operation/maintenance period thereafter,” writes Ho.

Additionally, iFast is leading a consortium which has submitted its bid for a Malaysia digital bank licence. Results for the five new licences should be released by Bank Negara Malaysia in 1Q2022. iFast will own a 40% stake in the partnership, which includes Malaysian partners Koperasi Angkatan Tentera Malaysia, THZ Alliance and Lee Thiam Wah, as well as international partner Yillion Fintech.

Likewise, DBS Group Research analyst Ling Lee Keng is maintaining “buy” on iFast with a target price of $12.93.

“We maintain our positive view on iFast on the back of the strong growth momentum ahead, propelled by the Hong Kong business from 2024 onwards. We expect more room for AUA growth. iFast is well poised to capture more market share in its key market Singapore, where its share is just 10% of the approximately $128 billion in AUM of the collective investment schemes,” writes Ling in an Oct 26 note.

Ling notes that trading activities were generally more subdued in 3QFY2021 compared to the earlier part of 2021. “For 9M2021, net profit accounts for 72% of our FY2021 projections, broadly in line as 2H2021 tends to be stronger based on the trend in the last two years, accounting for about 60% of the full-year contribution. 3QFY2021 net profit contributed to 23% of our FY2021 numbers.”

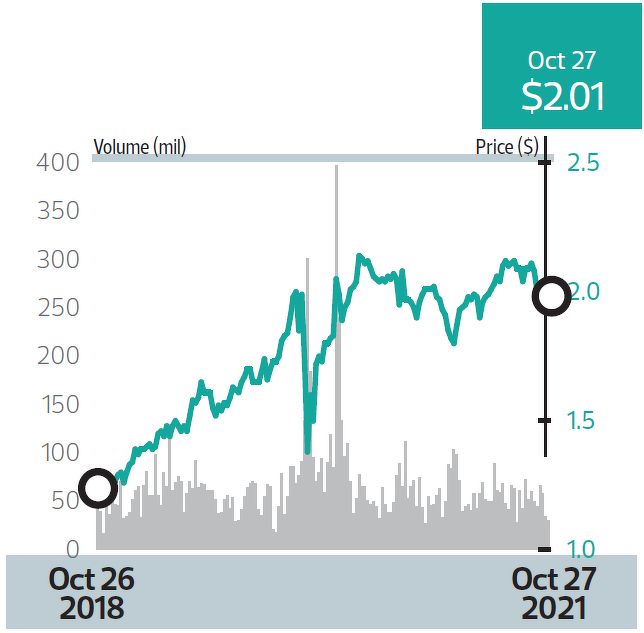

On the other hand, Citi Research analyst Tan Yong Hong holds a contrarian view, recommending investors to “sell” iFast as he sets a target price of $7.50.

iFast’s 3QFY2021 results missed consensus estimates due to slowing AUA growth momentum and ongoing platform margins pressure, writes Tan in an Oct 25 note.

“iFast has enjoyed strong net AUA inflows but we believe that could be at risk post-quantitative easing (QE) tapering,” says Tan.

iFast’s share price has risen more than 800% since mid-2020, notes Tan, and he thinks the market is pricing in too much upside from the upcoming HK eMPF project tender. “We estimate the market has priced in about $3 upside from this project, but our bottom-up approach suggests just 90 cents.” — Jovi Ho

Netflix

Price target:

PhillipCapital “accumulate” US$724

Squid Game and Money Heist pull in the cash for Netflix in 3Q21

While Netflix did not win the KRW45.6 billion ($52 million) prize money available in Squid Game, the hit series — along with Money Heist — has propelled the company to a strong showing in its 3QFY2021 ended Sept 30.

With this, PhillipCapital analyst Jonathan Woo has maintained his “accumulate” call on Netflix with an unchanged target price of US$724 ($975.76)

Woo notes that the company’s 3QFY2021 results are “above expectations”, adding that year-to-date FY2021 revenue and patmi is at 75% and 101% of his FY2021 forecasts respectively.

This was due to an increase in both paid memberships and average monthly revenue per membership (ARM). Woo highlights that there were 4.4 million paid net membership additions, a 99% y-o-y increase compared to 3QFY2020, almost 1 million more than the company’s projection of 3.5 million.

Most of the net additions came from the EMEA (Europe, Middle East and Africa) and Asia Pacific region, and the uptick in membership growth was due mainly to big hits like Squid Game and Money Heist, which brought in record viewership numbers.

Furthermore, the increasing membership base and price boosted 3QFY2021 revenue to US$7.5 billion, a 16.3% y-o-y growth. ARM ended 3QFY2021 at US$11.80, representing an 8% growth year-to-date, primarily due to price increases in the Latin America region.

Separately, there have been “strategic acquisitions by Netflix to boost content creation”. Woo writes: “We believe that selective acquisitions in the Roald Dahl Story Co and video game developer Night School Studio will boost its IP library for future content, as well as to improve its gaming capabilities to ramp up production of mobile video games.”

In terms of revenue, Woo notes that 4QFY2021 is seasonally the strongest quarter of the year, with strong growth in paid memberships and ARM.

“4QFY2021 should be no different, especially with this season’s scheduled introduction of new quality content, and price hikes. We expect to see a relatively large content slate arriving in 4QFY2021, after lighter 1Q and 2Q content slates due to Covid-related production rollovers in FY2020.”

Revenue is expected to be strong for 4QFY2021 at US$7.7 billion, but Netflix has softer q-o-q guidance for earnings per share (EPS) and patmi in 4QFY2021. Patmi is guided to stand at US$365 million, 75% lower q-o-q. Woo says this is led by a sharp increase in content costs due to a packed content release schedule, and EPS is expected to be US$0.80 for the quarter.

4Q EPS and patmi is typically weaker than the rest of the year, due to higher content costs associated with higher volume of content releases, Woo says. — Lim Hui Jie

Thai Beverage

Price target:

UOB Kay Hian “buy” 92 cents

ThaiBev ‘largely underappreciated’ by market with its ‘attractive valuation’

UOB Kay Hian analyst Llelleythan Tan has maintained “buy” on Thai Beverage (ThaiBev) with the same target price of 92 cents.

“We value: the spirits business at 17 times EV/Ebitda, lower than global peers; the beer business at 16 times EV/Ebitda, in line with Asean peers; the non-alcoholic beverages (NAB) business at 2.5 times EV/ sales; and the food business at 14 times EV/ Ebitda, in line with local peers,” writes Tan in an Oct 22 report.

“Frasers Property and Fraser & Neave, of which ThaiBev owns 29% each, are valued based on market value,” he adds.

Tan’s report comes after the Thai government announced its plans to reopen the country’s international borders to 10 countries to boost its battered tourism sector.

From Nov 1, vaccinated travellers from 10 “low risk” nations will be allowed to enter Thailand without the mandated seven-day quarantine restrictions.

Countries on the list include Singapore, the US, the UK, Germany and China.

According to the Thai prime minister, the list of countries may increase in December and January 2022 depending on the success of the initial phase of reopening.

The authorities are also looking into lifting Thailand’s ongoing alcohol ban in restaurants on Dec 1.

Bars and nightlife venues could also reopen amid the higher number of international tourist arrivals.

The way Tan sees it, the arrival of vaccinated tourists would help boost alcohol consumption and volume in the country.

“With 90% domestic market share for spirits, ThaiBev is set to experience an uplift in FY2022 spirits sales volume due to higher tourist arrivals and the relaxation of Covid-19 restrictions,” he writes.

“ThaiBev’s 9MFY2021 spirits sales volume remained resilient (+4.2% y-o-y) in spite of the Covid-19 pandemic, largely due to its commanding market share and roughly 95% of sales volume being off-trade,” he adds.

According to Thailand’s Office of Industrial Economics (OIE), 2021 year-to-date sales volumes for white and brown spirits in the country have recovered to 95% and 85% of pre-Covid-19 levels.

“Looking forward, with the arrival of vaccinated tourists in 1QFY2022, we think this would help support ThaiBev’s on-trade and off-trade spirit volumes from FY2022 onwards,” continues Tan.

Amid the reopening of entertainment venues along with the alcohol ban, Tan says he expects a stronger rebound for on-trade spirit sales volumes.

On this, he estimates that “a full recovery for on-trade spirit volumes would boost the spirits segment’s FY2022 ebitda and ThaiBev’s FY2022 net profit by 2.0–3.0% respectively”.

“As the spirits segment has historically contributed 85% of the group’s overall net profit, we reckon that upcoming favourable tailwinds for the spirits segment would help lift ThaiBev’s overall earnings moving forward,” he says.

On ThaiBev’s beer segment, a full recovery in on-trade volumes to pre-Covid-19 levels would see the segment’s FY2022 ebitda increasing by 1.5% to 2.0%.

“However, as close to 90% of ThaiBev’s beer segment net profit comes from Sabeco, we reckon that net margins expansion would instead be dependent on the reopening of entertainment venues in Vietnam, which remains closed, rather than Thailand. Thus, we see little impact on ThaiBev’s overall net profit,” writes Tan.

To this end, Tan sees ThaiBev as “attractively priced” at –1 standard deviation (s.d.) at its mean price-to-earnings and EV/Ebitda.

This, he says, is “backed by an expected earnings recovery underpinned by favourable tailwinds”.

“In our view, this [counter] remains largely underappreciated by the market given ThaiBev’s attractive valuation,” he adds. — Felicia Tan

Mapletree Logistics Trust

Price target:

UOB Kay Hian “hold” $2.08

CGS-CIMB “hold” $2.11

Unattractive yield prompt ‘hold’ calls

Analysts at UOB Kay Hian and CGS-CIMB maintain their “hold” calls for Mapletree Logistics Trust (MLT), citing unattractive yield versus other industrial REITs.

In an Oct 25 note, CGS-CIMB analysts Lock Mun Yee and Eing Kar Mei note that while they like MLT for its pan-Asian logistics asset focus, the FY2022F dividend yield of about 4.3% is on the lower end when compared to its peers.

The analysts have tweaked MLT’s FY2022F to FY2024F distribution per unit (DPU) estimates by 0.16% to 0.76%, aside from lifting its dividend discount model (DDM)-based target price to $2.11.

Meanwhile, UOB Kay Hian analyst Jonathan Koh has kept his DPU forecasts and target price unchanged at $2.08.

MLT reported a 5.7% y-o-y rise in 2QFY22 DPU of 2.173 cents. This was driven by a 25.2% y-o-y improvement in gross revenue due to higher contributions from existing properties, accretive acquisitions and income from the re-cently completed redevelopment of Mapletree Ouluo Logistics Park P2 in China.

Koh says MLT has achieved positive rental reversion of 2.4% for 541,370 sq m of new and renewed leases in 2QFY22, a slight pick-up compared with 2.2% in 1QFY22. The positive reversions were contributed by Malaysia (3%), Vietnam (3%), Hong Kong (2.6%), China (2.5%) and South Korea (2%). He adds that the retention rate was healthy at 91%.

MLT’s portfolio occupancy held steady q-o-q at 97.8% as at end-2Q. This was supported by higher occupancies in Singapore, Japan and Hong Kong, but moderated by lower take-up in China, Lock and Eing note.

They add that there were positive rental reversions of 2.4% coming across its geographic footprint, mainly from renewal or replacement leases, with the most uplift from Hong Kong, Vietnam, Malaysia, South Korea and Singapore.

“The trust has a remaining 14.6% and 28.5% of rental income to be renewed in 2HFY2022F and in FY2023F, respectively. Management highlighted that while there is expansion demand, tenants remain cautious on rent reversions. Nonetheless, we believe the positive reversion trend will likely remain intact,” the analysts say.

UOB Kay Hian’s Koh expects MLT to step up the pace of acquisitions in 2HFY22. It has announced three recent acquisitions, the first being Yeoju Logistics Centre in South Korea worth KRW235 billion ($271 million). The freehold property comprises two blocks of dry warehouses that were completed in 2019.

Fully leased to one of South Korea’s largest online fashion platforms and a domestic third-party logistics service provider, the acquisition will raise MLT’s e-commerce revenue exposure in South Korea from 24% to 31%, says Koh.

The second acquisition is of a cold storage facility in Melbourne, Australia, worth A$42.8 million ($43 million). The property, with net lettable area of 14,747sq m, comprises five blocks of cold and freezer warehouse, ambient warehouse and office. The property is 100% leased to Austco Polar Cold Storage, a wholly-owned subsidiary of Australian Securities Exchange-listed Wingara.

The last acquisition is of Mapletree Logistics Hub at Tanjung Pelepas, Malaysia worth RM404.8 million ($130.7 million). The property comprises two blocks of two-storey ramp-up warehouses and one block of one-storey warehouse. It is leased to multiple tenants, including Decathlon and Maersk.

Koh says MLT is pursuing acquisitions of logistics properties in China from sponsor Mapletree Investments and in Japan from third party vendors. The deal size for both transactions is expected to be substantial, he adds.

On top of acquisitions, MLT could potentially undertake asset enhancement opportunities in Singapore, the CGS-CIMB analysts highlight. “MLT’s gearing stands at 38.2% at 2QFY2022, providing the trust with good debt headroom to pursue inorganic expansion opportunities. MLT has only 3% of its total debt due to be refinanced in FY22 while all-in interest cost stands at 2.2%. — Khairani Afifi Noordin