Key to achieving these objectives is the importance of sovereignty. All of this is wrapped around the access to capital in ways that reduce sovereign risk and break the stranglehold of traditional financing.

We pick up from where we left off last week. The halted listing of Didi, the attacks on Tencent and Alibaba all seem to run contrary to the world leading growth of the Chinese tech and digital industry. However, these moves make sense when you accept that the role of the government is to restrain the excesses of capitalism and make it socially responsible and socially responsive.

Former Chinese leader Deng Xiaoping once said that “poverty is not socialism”. President Xi Jinping understands and agrees with this. But he may also well add that “socialism is not opulent extravagance.”

Against this background, the recent action in the digital economy reflects a growing concern about the adverse impacts of monopolistic behaviour by unrestrained capitalism.

They are effects most clearly seen in the American environment with the role social media played in the US insurrection. Chinese authorities are determined to avoid the same corrupting influence from social media giants and others who control big data collections.

Ironically, the data protection laws are modelled on the EU laws and require explicit customer consent as to how collected data will be used.

All of these policy moves take place under the umbrella of common prosperity. It is a newly revealed policy, but it has been the unifying force for some time because it is an essential part of moving towards a moderately prosperous society.

The West is keen to focus on the elimination of absolute poverty. Every time Western politicians want to be nice to China, they roll out platitudes about China’s successful war on poverty.

It is true, but it is only half the story.

China has done an expectational job in lifting people out of poverty but that does not address the issue of the expanding gap between the rich and the poor. The Gini coefficient is the standard measure of inequality, and the US and China are separated by four basis points.

However, in the US it is accepted that executive pay will be some 300 times greater than the average weekly pay packet.

The West reluctantly accepts that you should lift up the poor and push down on the rich by redistributing some of the wealth of the rich to provide social services. Of course, it is easier for the rich to find tax loopholes than it is for the poor to find opportunity.

China has lifted the poor, and now it is beginning to push down on the rich. In the West, we use a progressive taxation system, which is more like a leaky colander than anything else.

China does not yet have an effective taxation system so it is applying social pressure to these companies to voluntarily redistribute wealth.

There is an iron fist in this velvet glove but the philosophy behind the action is to reduce the gap and increase the equitable spread of wealth. This is what Xi means by common prosperity.

In time, this social pressure may be reduced with the implementation of a more effective and progressive tax system.

Underpinning that possibility is the China digital currency, which allows the instant collection of economic data at its most granular level.

Before we look at how this impacts on capital markets we need to consider issues of sovereignty. We will do this next week.

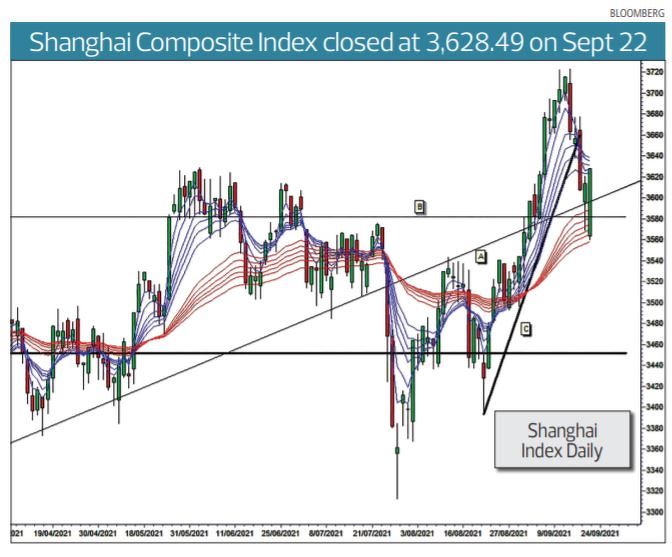

Technical outlook for the Shanghai market

The Shanghai market has been closed for the first two days of this week for the Mid-Autumn Festival.

After every fast rise there comes a fall and then, in this case, a very strong rebound. If the rally is to turn into a sustainable uptrend then the support level must hold and act as a base for a new rally.

The index over-shot the support levels, but then developed a very rapid rebound.

There are three support features in the Shanghai index chart, three of which failed. They are important because these are future potential resistance features which will determine how the rebound developers.

The first is the value of trendline C. This trendline defines the fast moving rally. The index crashed below this line confirming the end of the rally.

This line now has the potential to act as a resistance feature.

The short-term Guppy Multiple Moving Average (GMMA) has turned down and compressed, confirming the rally retreat.

For the potential longer-term trend we look at the role played by the longterm uptrend line A. This is the second support feature and was temporarily broken. This has variously acted as a support and a resistance feature. The index dipped below this level, but closed on the value of the line. Then it opened below the level but closed above the trend line.

This is typical of a market overshoot, or overreaction.

The horizontal resistance line near 3,580 has acted as a long-term resistance feature of the Shanghai Index. It is the upper limit of a long-term sideways trading band with a value near 3,580.

Unusually, this has not acted as a strong support or resistance feature in this retreat and rebound environment.

This is a strong rally with the potential to retest recent highs near 3,720.

Daryl Guppy is an international financial technical analysis expert and special consultant to Axicorp. He has provided weekly Shanghai Index analysis for mainland Chinese media for two decades. Guppy appears regularly on CNBC Asia and is known as “The Chart Man”. He is a national board member of the Australia China Business Council. The writer owns China stock and index ETFs

Photo: Bloomberg