Face is lost when you are not treated or acknowledged in a way that is befitting of your status or position. One obvious example is providing an inappropriate standard of accommodation for the chairman of a visiting investment delegation which makes him lose face.

However, there are subtler social situations which may lead you or your host to lose face. In negotiating a multimillion-dollar deal, you choose to stay in a four-star hotel to save cost. You think this choice shows you want to keep business costs down, which leads you to win face. Instead, the decision just shows how stingy you are so you lose face.

Here are a couple of other examples. The host loses face at a relaxed informal dinner if you order an extra bottle of wine because this suggests he is not aware of your needs. Face is lost when you offer to pay for the meal because it suggests your host does not have the necessary financial resources. Good friends may “fight” with each other over paying for a meal but this is definitely a no-no in a business environment.

The opposite is also true. Face is gained when you are treated better than expected. This goes beyond giving face because there is an acknowledgement of a change in status and that the relationship has entered a higher level. This higher level of treatment allows you to gain and keep face. This may come from an unexpected pickup from the airport by the chairman’s limo or you are reseated next to the host at a major conference or meeting. Face is gained not by what you do but also by the acknowledgement of what you have done. This is more than being praised. It is an acknowledgement of a change in your status.

See also: Taiwan may push back timeline to meet green energy goal after missing it last year

Face is received and acknowledged when you are treated in a way consistent with your standing in the group. As a foreigner at a conference, it is appropriate I speak English. I receive face because this is what is expected of me as a foreign expert. I give face to the organisers because I fill the role and expectations of a foreign expert.

Face is taken away when I speak entirely in Chinese at a conference. I take away my standing as a foreign expert. I do not lose face because the content of my delivery is high quality. I diminish my “foreign-ness” by speaking in Chinese and some of my face is taken away. I also caused the organiser to lose face because I am less foreign. I gain face with an introductory greeting in Chinese because this shows friendliness but I add to this face by switching back to English for the remainder of the speech.

The final wrinkles in face come from the intersection of face and guanxi or relationship. Face is transferred by association and introduction. It is both tangible and intangible. Chinese face is more pervasive than the casualness of the Singaporeans and it has a fluidity and complexity beyond the rigid formality of the Japanese. A better understanding gives you an edge in business and as business gradually resumes, this edge becomes significant in the more competitive environment.

See also: CK Hutchison seeks damages via arbitration on Panama Ports

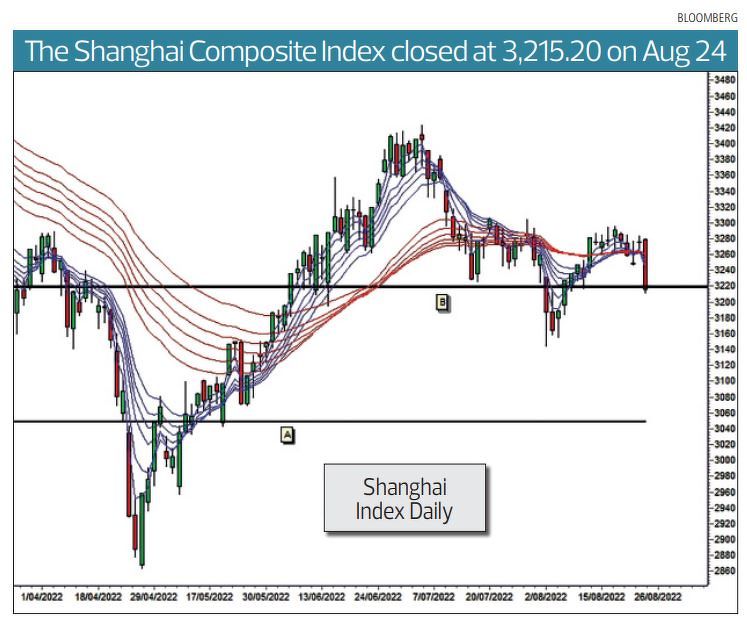

Technical outlook for the Shanghai market

The Shanghai Index breakout is continuing slowly with consolidation around recent levels. A fast fall is testing support near 3,220. While this slow-moving market does not satisfy traders, it was welcomed by investors because a slow breakout is often associated with the resumption of a stable uptrend. However, the rapid fall on Wednesday has broken the steady uptrend move.

The Guppy Multiple Moving Average (GMMA) relationships show diminishing downward selling pressure but not an increase in buying pressure. The long-term GMMA is moving sideways but has developed rapid compression. The compression shows a high level of agreement about the price of the index and the value of the index. Such periods of agreement about price and value are often followed by periods of significant disagreement. The sudden collapse back to support near 3,220 may suggest the disagreement is on the downside. It is the short-term GMMA or traders that provide evidence of the direction of the change in sentiment. They remain unclear in this environment.

The short-term GMMA has moved back to the long-term GMMA. This is not bullish but it is not yet a repudiation of the previous stronger bearish environment.

For more stories about where money flows, click here for Capital Section

The significant feature is the support level B near 3,220. This is not a well-defined level but this area has acted as a support and resistance feature. A successful retreat and retest of this level as a support feature confirmed the upwards breakout and the potential to move to the next resistance level near 3,380.

The level is undergoing a significant test so traders are alert for overshoot and rebound development.

A weak head-and-shoulder trend reversal pattern was developing and this was close to being invalidated by a move above 3,290. The failure to move above this level puts this pattern back into play with an extended right shoulder development. These extended developments have become a common feature of this pattern in recent years.

This was a weak breakout and it is under threat. A successful test of support will confirm an uptrend continuation. Failure of support for a retreat sees a downside target near 3,040. Currently, the market has no clear uptrend or downtrend.

Daryl Guppy is an international financial technical analysis expert. He has provided weekly Shanghai Index analysis for mainland Chinese media for two decades. Guppy appears regularly on CNBC Asia and is known as “The Chart Man”. He is a national board member of the Australia China Business Council. The writer owns China stock and index ETFs