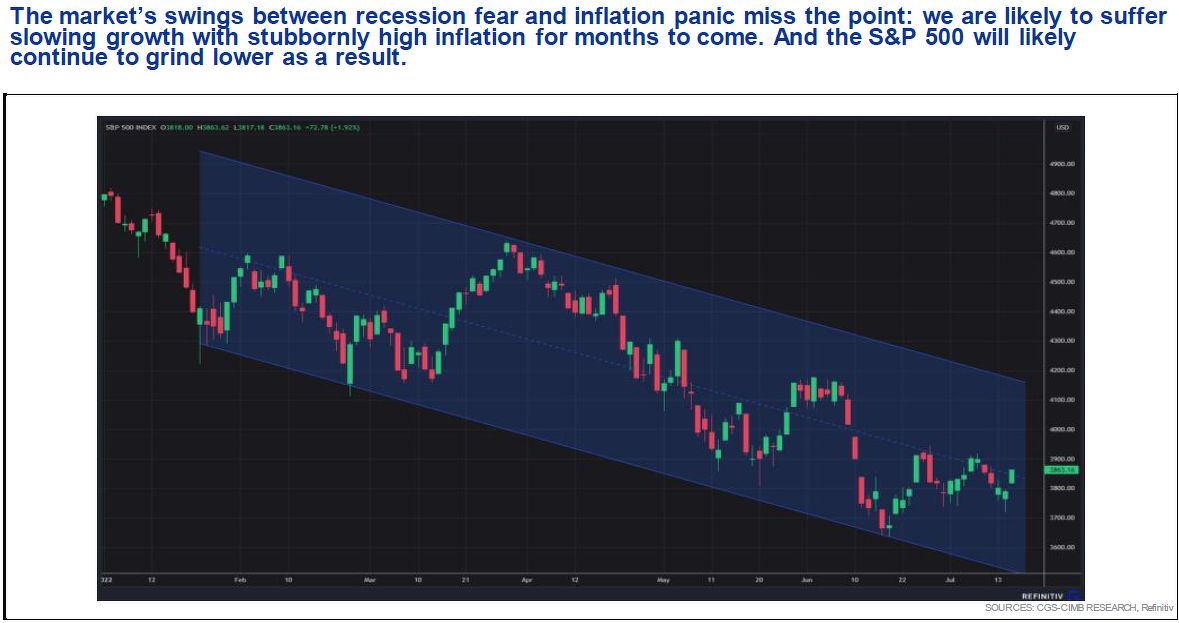

CGS-CIMB Research analyst Lim Say Boon is of the view that the global macroeconomic outlook will see slow growth and high inflation, saying in a July 18 presentation that this is the “likely outcome” from the usual time lag between demand destruction and sustained suppression of inflation.

CGS-CIMB Research analyst Lim Say Boon is of the view that the global macroeconomic outlook will see slow growth and high inflation, saying in a July 18 presentation that this is the “likely outcome” from the usual time lag between demand destruction and sustained suppression of inflation.

![[19/05/26] new top stories](/_next/image?url=https%3A%2F%2Fedgemarkets-transferred.s3-ap-southeast-1.amazonaws.com%2FPEO_KUNHEE_PARK_01_AC_2.jpg%3FTd3bG7fJqxPW3hMZRxhyfGgI25yRRD5v&w=640&q=75)