On the surface, there appears much for businesses to be concerned about: Biden’s campaign website promises doubling the minimum wage from US$7.25 to US$15 ($9.95 to $20.55) an hour and raising taxes on corporate America. UBS estimates that raising the corporate tax rate to 28%, alongside other proposed tax changes, would lower S&P 500 profits by 8%. Sean Markowicz, strategist at fund manager Schroders, sees a Biden presidency potentially increasing the appeal of non-US equities after years of US equities outperforming the rest of the world.

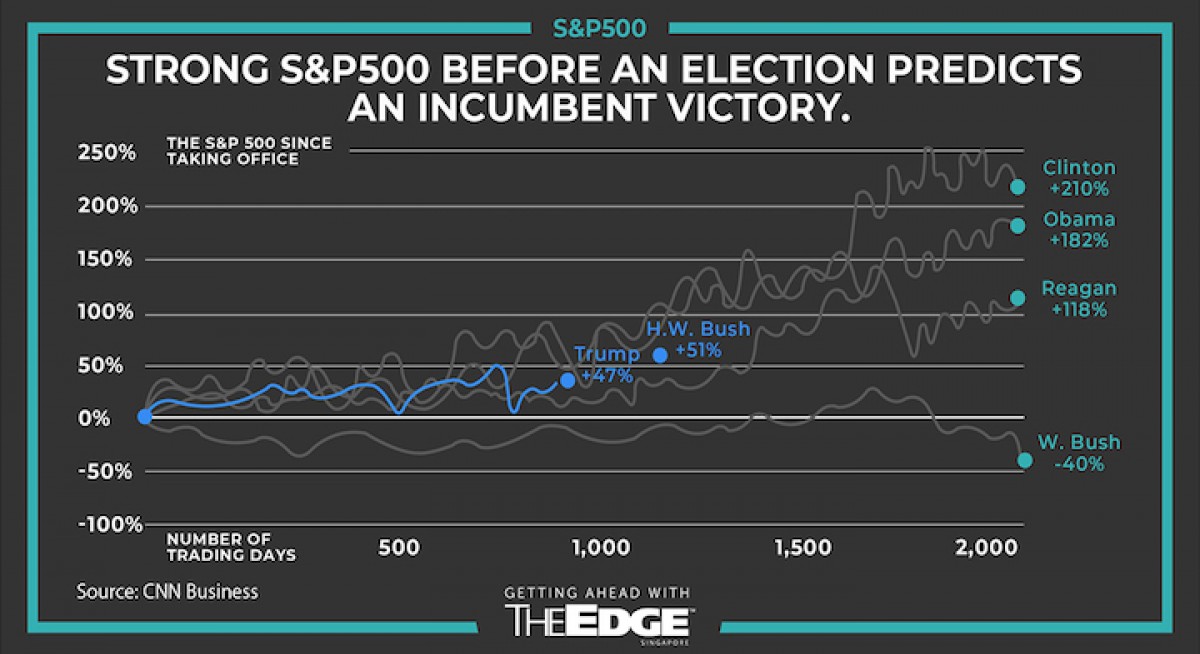

THE EDGE SINGAPORE - “I have been around for a long time, and it just seems that the economy does better under the Democrats than the Republicans,” said a puzzled Donald Trump in a CNN interview with Wolf Blitzer in 2004. Nevertheless, financial markets have often been wary of Democratic presidents, fearing that they would wield redistributive taxation to the detriment of profits. Wall Street welcomed Trump’s election with great jubilation in 2016 — the Dow rose 257 points to near lifetime highs as the Republicans gleefully contemplated the possibility of tax cuts and deregulation.

With some predicting that Democrats will likely win both the House and Senate, some observers fear that redistributive policies would put a significant downer on earnings. While BOS’ Eli Lee thinks Joe Biden as president would stabilise the US-China relationship, he believes that such an outcome would only be favourable with a Republican Senate, since they can use the Upper House’s “power of the purse” to avert a redistributive budget. A “blue wave” would be bad for investments, he says, with a second Trump term at least guaranteeing pro-business policies. DBS chief investment office (CIO) predicts that the Democrats have a 65% chance of winning the Senate.