But when demand for its products surged, its earnings skyrocketed in tandem. From US$41,000 in 3QFY2019, Medtecs’s net profit went to US$45.7 million ($61.05 million) in its 3QFY2020 ending Sept 30. Revenue, in the same period, was up 636% y-o-y to US$124 million. For the nine months ended Sept 30, Medtecs’s net profit surged 198 times to US$84.6 million, on the back of a 474% increase in revenue to US$287.2 million.

Medtecs’s record earnings helped drive up its share price from just four cents at the start of the year to an all-time-high of $1.85 on Aug 19, although it has since corrected to around $0.95 as at Dec 14. To share some spoils with its shareholders, the company also distributed its first dividend since 2007, with US$0.0085 per share paid following its 1HFY2020 earnings, versus just US$0.001 per share paid in 2007.

It was clear that for the healthcare workers, lab technicians and various other professions who are working round the clock to care for Covid-19 patients while working on a cure for the disease, they will need a lot of PPE in their jobs, especially rubber gloves.

Among the players entering the market to meet the demand include established names such as Top Glove, UG Healthcare and Riverstone Holdings. New entrants such as Aspen (Group) Holdings are also entering the fray.

See also: STI crosses 4,400 points, hits new high

Skyrocketing demand

In a broker’s note on the sector dated Nov 20, CGS-CIMB analyst Ong Khang Chuen said the Malaysian Rubber Glove Manufacturers Association (MARGMA) “remains upbeat” on prospects for the sector, and expects global rubber glove demand to reach 360 billion pieces in 2020.

This will be followed by a further 15% to 20% growth to about 440 billion pieces in 2021. And even with the Covid-19 pandemic fully under control, MARGMA sees “sustained growth in the coming years”, as there is a need to replenish inventory especially in neglected sectors such as F&B and electronics, amid overall increase in hygiene requirement.

Phillip Securities’s head of research Paul Chew expects demand to rise by about 90 billion pieces in 2020 and 2021, while production capacity is expected to increase by 70 billion pieces.

See also: From America to Asia, ‘timing is right’ for SGX measures: Ng Kok Song

MARGMA said that due to the supply shortage situation, current order lead times for gloves have risen to eight to 10 months, compared to one and a half to two months pre-Covid-19.

MARGMA believes that capacity growth will take time to catch up, as setting up a production line takes between one and one and a half years. In the meantime, glove makers will continue to enjoy higher selling prices, which is now at around US$70 to US$80 per thousand pieces of gloves, versus US$25 pre-Covid-19. When supply catches up, selling prices might still hover at 50% to 60% above pre-Covid-19 levels by 2023.

Even news of the vaccine will not stop the upward run that glove makers have experienced in recent months. “The vaccine in the medium term will not stop the pandemic. The pandemic is still raging globally and new daily cases doubled in just two months to almost 600,000 cases per day,” says Chew.

As the vaccine is deployed, Chew expects an improvement in demand from other sectors that were affected by lockdown or weaker economic growth such as food and beverage, retail, airlines and manufacturing.

Ong has a stronger preference for Riverstone Holdings, given its “relatively cheaper valuation and our expectations of higher normalised profits backed by a 59% y-o-y manufacturing capacity expansion in 2021.”

Riverstone Holdings reported a revenue of about RM626.7 million ($205.5 million) for its 1HFY2020 ended June 30, a jump from the RM480.2 million from the same period last year. Most notably, profit before tax more than doubled from RM74.1 million to RM175.7 million. More recently, in a business update, Riverstone Holdings has reported 3QFY2020 revenue of RM482.3 million, a y-o-y jump of 92%, and gross profit of RM251.6 million, up 389.6% y-o-y.

Looking ahead, the company’s adding more lines and is on track to raise total production capacity by 1.5 billion pieces to 10.5 billion pieces of gloves annually by end 2020 and 12 billion pieces by end 2021. Riverstone also says that the additional output from the new capacity has been spoken for.

To stay ahead of Singapore and the region’s corporate and economic trends, click here for Latest Section

It is a largely similar story over at UG Healthcare. For its 1QFY2021 ended Sept 30, attributable profit shot up by 74 times y-o-y to $22.7 million, while revenue in the same period increased by 2.7 times to $71.2 million. To reward shareholders, UG Healthcare has declared a final dividend of $0.00238 per share for FY2020. The company did a one-to-three share split on Oct 2. This means shareholders are getting nearly three times as much as that paid for FY2019, when $0.00259 per share was paid.

The company has also brought forward its expansion plans, raising a planned increase of 300 million gloves in March 2021 to 500 million gloves, giving it an annual capacity of 3.4 billion gloves.

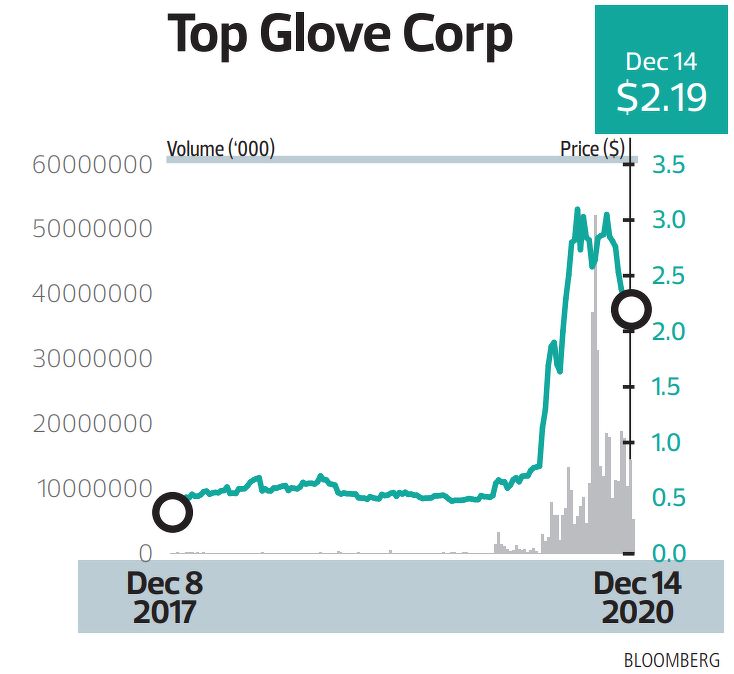

Top Glove under scrutiny

As the world’s largest glove maker, Top Glove has enjoyed a stellar year. Revenue for its FY2020 ended Sep 30 surged 51% to RM7.2 billion compared with the previous financial year, and net profit for the full year jumped from RM367.5 million in FY2019 to RM1.79 billion.

4QFY2020 revenue jumped to RM3.1 billion from 4QFY2019’s figure of RM1.18 billion, while profit after tax for the same period skyrocketed almost 18 times y-o-y, from RM74 million to RM1.32 billion.

Dividends have also swelled accordingly. Top Glove declared a dividend of 8.5 sen per share in 4QFY2020, bringing the total dividend payout for FY2020 to 11.8 sen per share, almost five times the 2.5 sen dividend paid in FY2019.

Investors chased Top Glove’s share price to a record high of $3.13 on Oct 19, although it has since eased to $2.19 as at Dec 14.

More recently, in its 1QFY2021 results, the company announced a record dividend of 16.5 sen for this quarter alone, far exceeding the full year dividend for FY2020. The total dividend payout stands at 56% of profit, which exceeds its established dividend payout policy of 50% and includes a 6% special dividend.

For 1QFY2021, Top Glove achieved a revenue of RM4.8 billion, up 294% y-o-y, and up 53% quarter-on-quarter. Attributable profit surged by 20 times to RM2.4 billion y-o-y, and doubled against 4QFY2020.

However, the stellar financial performance was marred by news that many of its own workers were infected by the virus recently. This forced the company to halt work at 28 of its plants so as to stem the spread of the virus. As of Dec 8, the company has a total of 5,147 workers testing positive for Covid-19, although it added that about 90% of them have been released from hospital and are fit for work.

The company also found itself under scrutiny after Malaysian authorities said in December that it would file charges against Top Glove because of poor worker accommodation. Earlier, the US had added rubber gloves produced in Malaysia to a list of products produced by forced labour. In response, Top Glove said it was working to address those concerns by improving existing worker accommodation. This is expected to be completed by Dec 31, the company added.

With the sky high profits earned by existing glove makers, it is no surprise that new players want to join in and carve out a slice of the enlarged pie.

New challengers

Aspen — which is better known for its property developments in Penang — has set up a glove-making joint venture, targeting an initial capacity of 1.6 to 1.8 million gloves per annum, before growing to 6.5 to 7.1 billion gloves by the end of 2022.

In a presentation on Oct 14, the company said it will first focus on manufacturing medical examination gloves, before moving into surgical and speciality gloves. Eventually, it projects its annual capacity to be 26.4 to 28.1 billion gloves per annum in 2025.

And as with most glove makers, the news of Aspen expanding into this sector sent its share prices to record highs. Aspen listed back in July 2017, but from the IPO price of $0.23, its share price dropped to as low as four cents earlier this year. News of its planned diversification in August, however, sent it surging to as high as $0.335 on Aug 24, before closing at $0.22 on Dec 14.

For its 1HFY2020 ended June 30, the company reported losses of RM13.8 million, compared to a RM9.2 million profit in the year earlier, as the movement control order in Malaysia delayed progress of its projects.

Still, Aspen’s president and group CEO Murly Manokharan remains optimistic. In an earlier interview with The Edge Singapore, he said: “We have never been in the red [for our full financial year] in our entire history, and we manage our cash flow and operating costs very stringently. So, we are intervening and putting a lot of effort to be in the black for FY2020.”

Still, Aspen’s president and group CEO Murly Manokharan remains optimistic. In an earlier interview with The Edge Singapore, he said: “We have never been in the red [for our full financial year] in our entire history, and we manage our cash flow and operating costs very stringently. So, we are intervening and putting a lot of effort to be in the black for FY2020.”