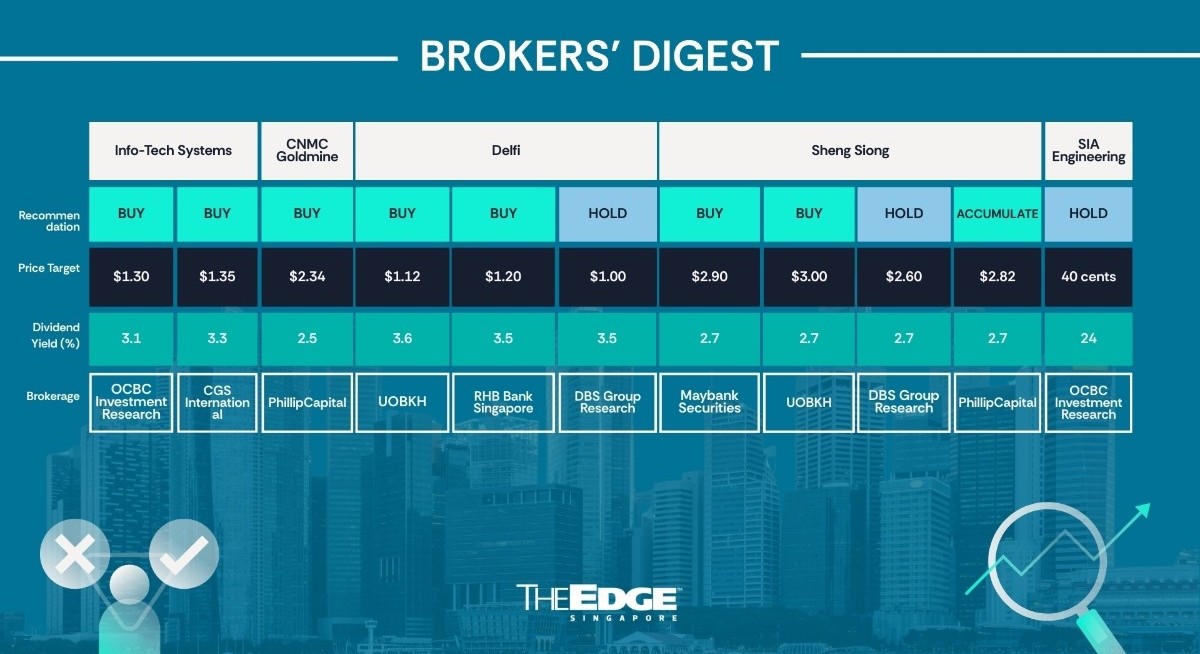

Ada Lim of OCBC Group Research has raised her fair value for Info-Tech Systems (SGX:ITS![]() ) after the business software provider reported better-than-expected full-year results for the first post-listing period. From an initial fair value of $1, Lim, who has kept her “buy” call, now figures that this stock is worth $1.30.

) after the business software provider reported better-than-expected full-year results for the first post-listing period. From an initial fair value of $1, Lim, who has kept her “buy” call, now figures that this stock is worth $1.30.

Info-Tech Systems

Price targets:

OCBC Group Research ‘buy’ $1.30

CGS International ‘add’ $1.35

AI-driven demand ahead