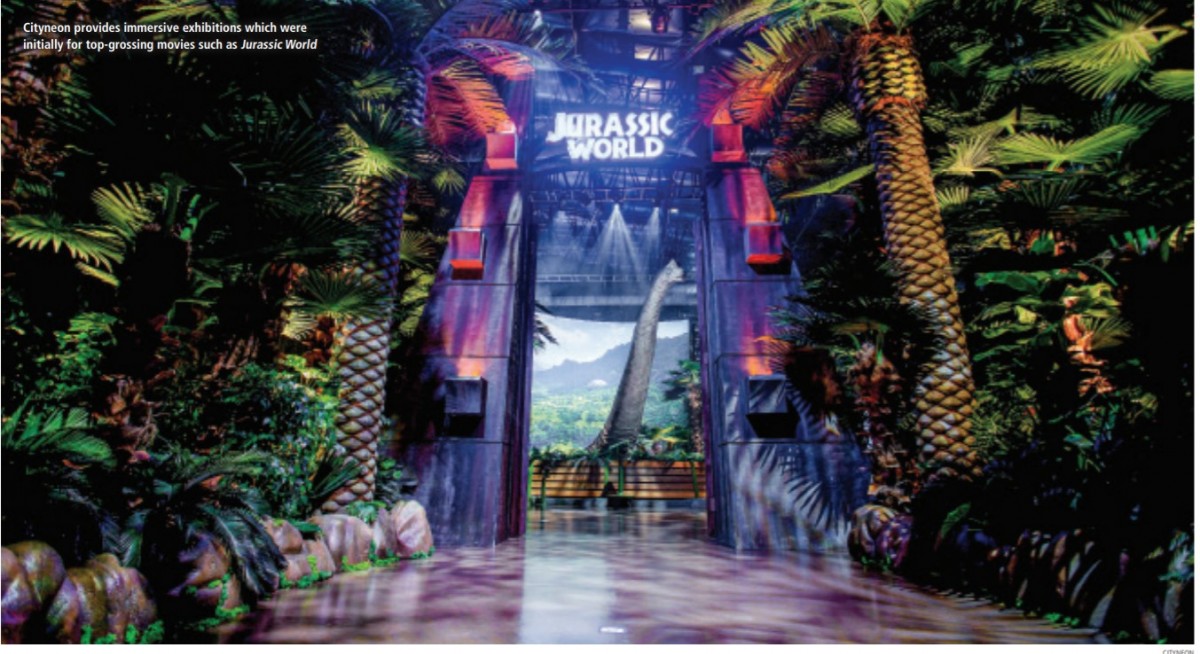

Still, some private companies restructure in the full glare of the public. Take Cityneon Holdings, the provider of immersive exhibitions, for example. Though privatised in 2018 at $318 million in a buyout by its executive chairman and CEO Ron Tan and Hong Kong businessman Johnson Ko, the company now has a business model which puts it squarely in the public spotlight.

Staying private means flexibility for companies to restructure while going public unlocks value for shareholders. But what the downsides of each plan?

Private markets — as the name suggests — provide privacy for companies wishing to grow or restructure away from the prying eyes of investors, without having to provide all the details that corporate governance and regulations require that they disclose.